ViTrox: How to Poop Up a Stock!!

Wednesday, October 11, 2006

Imagine.

Say you have a stock that has just broken up broken its base of 0.60 and is now trading around 1.05. And this stock price appreciation was done in less than one month time.

Now imagine, you are an analyst and you are asked to give a positive comment on the stock. And of course a high Target Price for the stock.

And to make matters worse, this stock was just listed recently and back then, folks gave it an IPO fair value of just 36 sens. Remember stock is now trading at 1.05 ok?

Just imagine.

Now say this stock is earning some 2.4 to 2.5 mil per quarter. So for current fiscal year, this stock should earn some 9-10 million for its 2006 fiscal year.

Are we ready to begin our task?

Just imagine the following conversation between A (the writer) and B (the Bossie).

A: Bossie, I know how. I shall project fy 2007 earnings at 18.8 million for this fella. Is it enough?

B: Are you nuts? This is not going to cut it.

A: Not enough. I project the next fiscal year earnings, fy 2008, to be at 27.9 million. Is that enough?

B: Ahh... you are getting smarter each day. That's it, that's the ticket!! 27.9 million it is!! Make the target price as high as possible!

A: Ok Bossie. 1.80 enough?

B: Good boy!

Incredible isn't it?

Me think so too!!!

Look at what it is happening here.

Vitrox. A year ago.

- ViTrox fair value at 36 sen

September 10 2005

SHARES of ViTrox Corp Bhd, a maker of systems that help chipmakers inspect their products, should be fairly valued at least at its reference price of 36 sen apiece, two research houses said.

The company, which is en route for listing on Malaysian Exchange of Securities Dealing and Automated Quotation Bhd (Mesdaq) Market on September 12, had issued 17.6 million new shares of 10 sen each at 60 sen per share.

However, it has also offered a 2-for-3 bonus issue and these bonus shares would also start trading on the first day, which means the theoretical ex-bonus price is 36 sen.

SBB Securities Sdn Bhd has given a fair value of 36 sen a share for ViTrox while Jupiter Research put a fair value of 43 sen, a 19 per cent premium over its reference price.

Here is how ViTrox has traded..

See how nicely ViTrox has appreciated lately? The stock went zoom, zooming from 60 sen base to 1.04.

And this morning, I saw this Kenanga research on it. Well, for a stock that had clearly appreciated so much, I find it so incredible that Kenanga has managed to write such a positive write-up on it.

Here are the main points it made.

- Home grown technology dynamo

Company Report BUY RM1.04 Initiating Coverage (Target: RM1.80)

12 October 2006

l A home grown technology dynamo which is gain significant market acceptance in Asia Pacific region, Vitrox Corporation Berhad ("Vitrox") is the leading machine vision solutions provider in Malaysia, catering particularly to the semiconductor industry.

l Rising trend of integrated circuit ("I/C") consumption especially in consumer electronics should continue to underpin demand for automation equipment and hence machine vision inspection system s.

l Three champion products namely machine vision system, automated optical inspection ("AOI") and electronics communication (I/O cards) hardware should propel growth going forward, underpinned by strong value propositions in terms of price / performance to the end clients .

l Extremely vibrant growth outlook with the company expected to grow a staggering 72.3% CAGR between 2006 and 2008 as the company’s new key products namely, AOI and gained traction in the market place.

l Outstanding profitability with net margins of 40% and above as company leverage on its intellectual property in addition to 12-year tax free pioneer status.

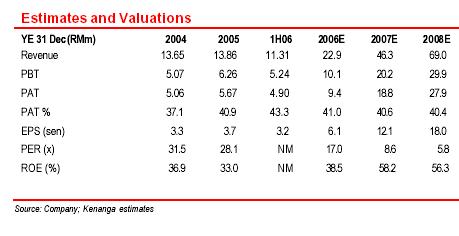

l Initiating coverage with a Buy. Our 12-month target price for the stock is RM1.80 using a 10x FY08 P/E instead of 8x given its explosive growth.

Catalysts including (1) Rising demand for automation equipment, (2) strong value propositions to end clients in terms of price / performance / back-up service and (3) sterling CAGR of 72.6% in the next two years.

See how the 12-month target price is at 1.80 and is based on FY2008 earnings estimates?

Well have a look at the table below to see how nicely they project this fy2008 earnings.

0 comments:

Post a Comment