Do you think privatisation is a healthy trend?

Friday, September 1, 2006

The privatisation of Worldwide Holdings.

As asked in earlier posting, do you think that is this a healthy trend?

Let's take a simple look at the recent proposal made to privatise Worldwide Holdings.

Let's not complicate matters and let's keep the issue is simple. Let's do this exercise from a simple reverse angle. Assume we are a potential buyer and assume that we, owns no shareholding (easier to see if viewed as a whole and when done, just count back the percentage) in this stock. And the objective of this exercise is to see if we are getting a good deal for this exercise or not. Let's see how profitable it is.

1. The crown or the moola in Worldwide is its shareholding of 20% in Genting Sanyen power plant (GS). Simple counting again. Just count how much this plant is contributing per quarter.

How much is this power planting contributing to Worldwide each year?

The above snapshot is taken for Worldwide's last fiscal year Q4 quarterly earnings. As can see from that table reported by Worldwide, GS is contributing some 57.461 million per year.

So if we buy Worldwide, we effectively buy the rights to receiving this 57.461 million per year!

This is what Worldwide gets. It's like rental money from its ownership in GS. How you want to value it?

Let's do some simple counting. Let's assume that we can get fixed deposit rates of 4% per annum. To get the equivalent of 57.461 million, how much would we need to deposit?

Answer?

Are you ready? How about 1436.53 million!!!

Now get this.

Do you reckon it is a good deal to pay 3.50 per share for Worldwide?

Now, Worldwide has some 177 million shares. So assuming we buy the whole company, we would need to pay 177 * 3.50 or some 619.5 million!!

And by paying 619.5 million, we get to keep that 57.461 million per year.

Which is a better deal? You tell me.

2. Just by buying Worldwide, we are already getting such wonderful return of investment from the money received from GS.

What about Worldwide Holdings itself? Worldwide is not an empty company.

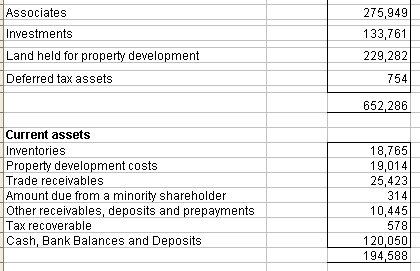

* Cough* Its piggy bank cash is worth some 120 million wor.

How? Is this free money? Take a look at Worldwide's last fiscal year Q4 assets stated in its quarterly earnings report.

Based on 177 million shares, the cash per share is already worth some 68 sen.

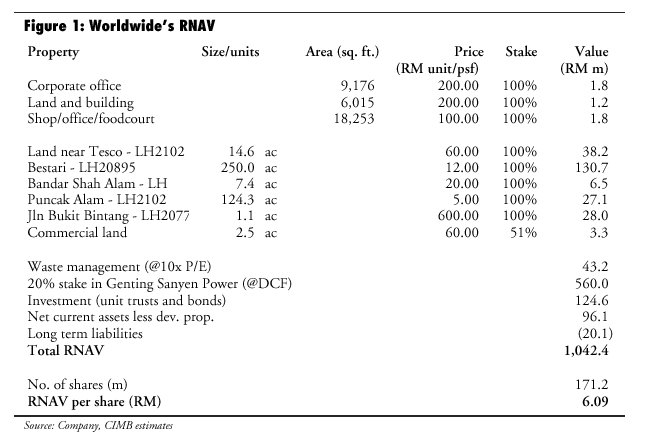

3) And what about it's landbank? CIMB on 4th April 2006, wrote on this stock. This is how it described Worldwide's landbank.

See that nice piece of 1.1 ac land on Jalan Bukit Bintang? See CIMB's valuations?

4) And what about it's waste management business?

So if we offer 3.50 for Worldwide, which effectively values Worldwide at 619.5 million, frankly speaking, do you think we are getting a good deal? We get the rights to receive some 57 million a year from the power plants, we get to keep the company cash, we get the land banks and also we get to have a waste disposal business too?

Don't you think we are getting an extremely out of the world deal of a lifetime?

And oh... so do you think privatisation is a healthy trend?

0 comments:

Post a Comment