Crest Builder

Monday, August 21, 2006

Crest Builder just announced its earnings. It's impressive..

Crest Builder Holdings Bhd (8591.KU) - Malaysia

2nd quarter ended June 30:

Figures are in Ringgit (MYR).

2006 2005

Revenue MYR54,119,000 MYR63,443,000

Pretax Profit 6,590,000 5,464,000

Net Profit 3,695,000 2,923,000

Earnings Per Share 3.00 Sen 2.60 Sen

Dividend Omitted Omitted

6 months ended June 30:

Revenue 113,017,000 116,893,000

Pretax Profit 15,248,000 12,844,000

Net Profit 9,322,000 8,048,000

Earnings Per Share 7.70 Sen 7.10 Sen

Dividend Omitted Omitted

Crest Builder closed at 0.97 sen. Down 2 sen.

Ok, so what's wrong?

Crest Builder current earnings of 9.322 million for its first 2 quarts of current fiscal year its much more than what Crest Builder did last fiscal year same period. Crest Builder managed 8.048 million for last fiscal year.

Well..

Remember this blog posting: Ze Numbers Game: II

So Crest Builder although doing 'ok' and perhaps 'good' with half year earnings totalling 9.322 million but just how good is this earnings when OSK numbers is projecting an astonishing earnings of 41.3 million for full year fy 2006!!!!!!!

So what do we have??

Ahem.. 'lost' research report.. amazingly 'flying sky' earnings projections...

Have a read again:

Back in April 2005, OSK wrote about Crest Builder. Price back then was 1.44. OSK gave it a price target of 2.59.

And I wrote that blog posting, Ze Numbers Game on Nov 2005.

Here is an extract of what I had written then.

<=============>

And this is how OSK valued Cresbld:

- However, by taking into account only the basic shares outstanding, we obtained a fair value of RM2.59 based on FY06 earnings, which provides an upside of 72.7% to its current share price.

ahem!

See onot?

And they based it on fy 2006 earnings! Earnings which went bang! bang! bang! like this below:

15.5 -> 16.2 -> 26.7 -> 41.3 -> 50.7million.

Fiyoooh... 41.3 million!!!

Incredible isn't it?

2005 FY projections is already perhaps a bit too optimistic at 26.7 million... but no... OSK did not based their valuations upon those numbers but instead they based it at an even more optimistic earnings of 41.3 million!!!!!!!!!!!!!!!

Now wouldn't u say that this is a bit too optimistic?

And when they make such optimistic projections, this simply allows them to create a stock with such a great upside potential (72.7% wor!) when they make their so-called BUY recommendation!

ps. Cresbld closed at 0.795 today. (back in Nov 2005)

<=============>

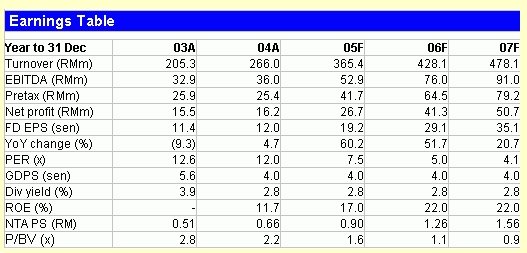

And how did Crest Builder did for its fiscal year 2005? Well have a look at its last reported quarterly earnings on Feb 2006.

Crest Builder made a net profit of only 12.198 million.

And how did OSK played ze number game?

Well the table below says it all...

OSK had projected an earnings of 26.7 million! Crest Builder only made a net profit of only 12.198 million.

Now check this out, today OSK has a brand new report on Crest Builder again.

Price of Crest Builder is now 1.12 and OSK has given it a 12-month target of 1.49.

LOL!!!... yup... just 1.49! (ps. In April 2005, Price back then was 1.44. OSK gave it a price target of 2.59!)

Wait... check this out too.

Ahem.. can you see that they have projected an earnings of 31.9 million for Crest Builder's fy 2006 earnings and an earnings of 35.2 million for its fy 2007. (last April 2005, OSK projected 41.3 million!! Does this mean they are less optimistic? LOL!)

And as stated in OSK own table, this translates to a 161.7% increase in earnings for this fiscal year!

So for a stock that had a whopping decline of 25% in fy 2005, is projected to grow 161.7% this fiscal year.

Highly incredible, isn't it?

Now check this out also...

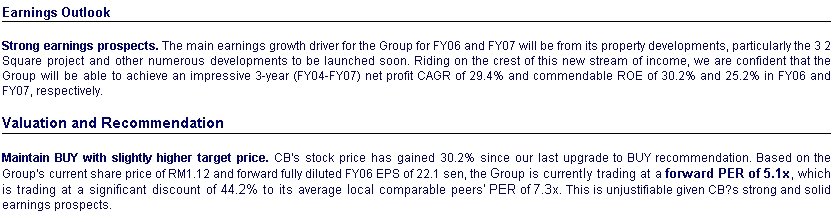

The below is a screen-shot of their reasoning...

Did I miss a report on Crest Builder since last April 2005? This is because the writer is saying:

- CB's stock price has gained 30.2% since our last upgrade to BUY recommendation.

Ps... does someone have a copy of that report? ... cos I find it really strange since I can't even search for this report in their archives.

- Group is currently trading at a forward PER of 5.1x, which is trading at a significant discount of 44.2%

It would be good to note that it is CHEAP because their forward PER of 5.1x is based on an earnings which is projected to grow 161.7% this year!

LOL!! Any stock which can grow so much would surely be cheap. Yes or not Shirley?

:D

0 comments:

Post a Comment