Regarding Scomi Group again.

Friday, August 18, 2006

Dedicated to The Killer! :-)

On 6th May 2006, I wrote the following:

I had actually made a posting on Scomi Group before. Let me reproduce what I have written on it. ( Sorry dude, it's just have gottabe long! )

<<==>>

Firstly, I have to say this. IPO subsribers to SCOMI would be really darn please with their investment if they held the stock from the start to now!

Scomi was offered to the public at a price of 1.38. Listed on May 2003.

In April 2004, there was a 3 for 5 bonus issue and then a 1 into 5 stock split.

- 08/04/2004 Entitlement - Others

For illustrative purposes, a shareholder holding 100 ordinary shares of RM0.50 each in SCOMI on the Entitlement Date shall be entitled to 60 ordinary shares of RM0.50 each in SCOMI pursuant to the Bonus Issue. Subsequently, his/her entire 160 ordinary shares of RM0.50 each shall be subdivided into 800 new ordinary shares of RM0.10 each in SCOMI.

So say, for simple illustrative purpose, someone subscribed to 5,000 shares of Scomi at 1.38 during Scomi's IPO, their capital outlay will be 1.38x5 = 6900.

So after the stock bonus, this investor would now hold 8 lots of Scomi. And after the stock split, the investor would be having 8x5 = 40 lots or 40000 shares.

So at closing price of 1.17 (this was the price of Scomi on 3rd Sept 2005), this investor's investment would be worth 46,800.00.

Which is really a darn good investment return!!!

And the picture below says it all!

So how did Scomi do since its listing?

For its fiscal year 2003, Scomi Group announced an earnings of 14 million.

For its fiscal year 2004, Scomi Group announced an earnings of 61.4 million.

Absolutely commendable. In fact, some would call it as brilliant!

So for the IPO investor, buying the stock of Scomi is looking at his/her company's net profit grow from 14 mil for fy 2003 grow to a very impressive 61.4 million for fy 2004.

Basically, isn't this what we all want in a company when we invest in it?

The company is making more and more moola each year!

Rite?

Now the question is or rather the issue is, we all know that Scomi is growing explosively via acquisition of companies or some would cynically call it the engineering of profits via acquistions.

Anyhow, I guess it would do no harm and it would makes sense if we dig deeper, rite?

And this can be done via some simple observation of its quarterly performance. Just some simple comparison of some key figures.

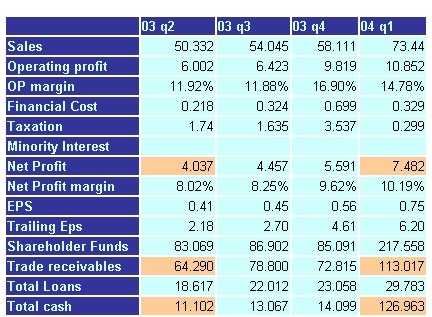

At the start (03 Q2 ), we were looking at a company with the following characteristics...

- Company was making about a quarterly net profit of 4 million.

- Cash was 11.102 million versus Total loans of 18.617 million. (a net debt position of 7.515 million)

Next we look at 04 Q1...

- Company is now making around 7.4 million per quarter. Fantastic.

- Cash is now 126.963 million with loans of 29.783. (net cash of 100.180 million). Fantastic.

- Slight worries. Trade receivables is now 113.017 million.

A very interesting footnote was found in the cash flow statemtent:

- 125 million was generated VIA SHARE PLACEMENT EXERCISE and entered into the company's piggy bank.

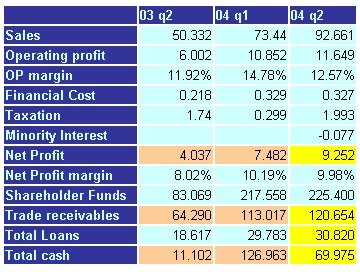

Now we are looking at 04 Q2.

Good points.

- Net profit is now 9.252 million. Just the same quarter, a year ago, Scomi was just a company making 4.037 million. Company is making more money isn't it?

- Cash stands at 69.975 million versus total loans of 30.820 million. (A net cash position of 39.155 million).

But here comes the worrying part..

- Trade receivables is now at 120.654 million. (Hmmm... a worrying signal? Hard to say at this moment of time cos after all this quarter Scomi showed a sales revenue of 92.661 million.)

- Cash flow. Starting cash was at 126.963 million. A quarter after a share placement issue, in which Scomi generated 125 million in this fund raising exercise. At the end of the quarter, cash is only at some 69.975 million. Where ze Moola go???? (ah ze classical arguement of a company using leverage to expand and grow the company!)

Scomi reported that earnings on 11th Aug 2004.

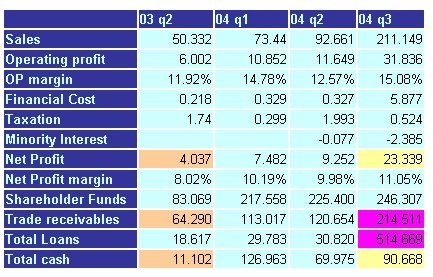

Let's watch happens in Scomi's next quarter, 2004 Q3.

Good point:

- Net profit is now 23.339 million. 5 quarters ago, Scomi was just a company making 4.037 million. Company is making more money isn't it? Isn't this what u call explosive growth?

Fantastic isn't it?

And again, here comes the worrying part...

- Trade receivables is now at 214 million. (Hmmm... again a worrying signal? And again hard to say cos Scomi had sales revenue of 211 million for the quarter and since with the company made making more sales, more receivables is accumulated, rite?)

- Cash is now at 90.668 million but the loans is now 514.669 million. Scomi is now in debt of 424 million!!!! ( A huge worry? )

A flag has been raised, eh? Them same old worrying issues is getting more worrying, isn't it? Time to exit da bugger?

Scomi reported that set of arnings on 3rd Nov 2004.

Next quarter, 2004 Q4 was pretty dull. Pretty much the same old, same old. A neither here or there quarterly earnings report.

So fast forward to 2005 Q1 earnings. Which was really 'interesting'..

Soooooo many issues!!!

1. Net Profit is only 14 million? Big worry? Down from 20+ mil on a q-q basis... (ahh.. again... some will argue cos on a y-y comparision.. this 14 million net profit is still much better than the 7 million it earned a year ago).

2. Trade receivables is now 333.889 million. Now this trade receivables is NOW a huge worry cos quarterly sales is now 229.236 million only. Where is that extra 100+ million of receivables coming from? What if a huge portion of these trade receivables turn bad? Bad debts then?

3. Loans? Loans is now 457 million. Down from 540 million a quarter ago.

4. Total cash increased to 118 million from 86 million a quarter ago.

5. Is 3 and 4 a good point? My answer is NO. If one looks at Scomi's Cash flow, Scomi's made yet another share placement to raise cash. A placement which saw Scomi raised 145.476 million.

So what we have is:

Scomi raised cash from placement of shares which is then used to pay off some of its loans....

But how does one evaluate Scomi's earnings performances? Surely if one is a buyer of Scomi's placement shares, one would probably not be too happy with it cos the bottom line is Scomi's net earnings declined from 20+ million to just 14+ million.

Now given 1,2, 3 and 4 and most importantly point 1, Isn't the time to really to exit this bugger?

Scomi reported this earnings on 25th May 2005.

Scomi closed at 1.40 on 25th May 2005.

And here comes the company most recent earnings (in Sept 2005)

And how did Scomi do?

1. Net earnings came in at 13.351 million. Which was down from 20 million plus earnings it earn a couple of quarters ago...

Now why issit such a huge worry?

1. Trade receivables is now a whopping 374 million.

2. Loans. Total loans is now 511 million.Up from a total loans of 457 million a quarter ago. Hmmm.... if one looks at the bigger picture, Scomi did a placement, paid of some 80 million plus in loans but come the next quarter, it borrows yet again. Doesn't it mean that Scomi is now back at square one? At the peak, Scomi total loans once stood at 540 million!!!

How? Now Scomi has been on a sell-off since May. Down some 30% and it is not too surprising eh?

Let's re-examine what has been said.

At the start (03 Q2), we were looking at a company with the following characteristics...

- Company was making about a quarterly net profit of 4 million.

- Cash was 11.102 million versus Total loans of 18.617 million. (a net debt position of 7.515 million)

8 quarters later, after countless of acquisitions and 2 share placement and sooooooo many ESOS....

We are now looking at....

1. A company making 13 million per quarter.

Compare to the 03 Q2 in which Scomi made only 4 million. An increase of 9 million So company is making 3.25 times more moola.

2. Company cash balance is now 106.119 million. Total loans stand at 511.613 million. Company is now in a net debt of 405.494 million.

Comparison. In Q2, company net debt position was a mere 7.515 million. Now the net debt position has increased by a WHOPPING 53X.

Justifiable given its current earnings? (some would ask: Does it make sense to increase ur total debt position by 405 million to make that extra 9 million in profit???? )

how? how? how?

Would it be wrong to say that this is an insane strategy employed by Scomi????

Oh btw, Scomi now has 991,130,700 shares. How signifacnt is this? Well, back in 03 Q2, Scomi Group had just around 91 million shares! ;p

<<==>>

That was back in Sept 2005. Sorry mate to bore you with all those details but I do reckon that it is useful to understand why Scomi rose so high and why its share price was declining quite a lot late last year (Scomi traded as low as 0.95 back in Nov 2005!).

Anywayyyyyyyyy...

In Nov 2005, Scomi announced its Q3 earnings. Scomi quarterly net earnings increased to 16 million.

In Feb 2006, Scomi announced its Q4 earnings. Scomi quarterly net earnings increased to a whopping 109.539 million!!!

So let's look at how did Scomi do since its listing...

For its fiscal year 2003, Scomi Group announced an earnings of 14 million.

For its fiscal year 2004, Scomi Group announced an earnings of 61.4 million.

For its fiscal year 2005, Scomi Group announced an earnings of 151.692 million.

And there you have it mate, yes it is true that Scomi has an astonishing growth rate!

But how about them points again? Well, as at its last reported earnings...

- Cash is at 87.595 million.

- Trade receivables has increased to 438.430 million.

- Group's borrowings is not at 918.363 million.

And yes, I do understand your issue that leverage can be used to generate a much higher revenue but on the other hand, I do hope you realise that this leverage issue is a matter of personal views and opinions. Me, for one, believe that too much leverage can turn deadly if one is not prudent enough.

And by the way, from my live quotes, I do note that as of today, Scomi Groups' number of shares is now 996.208 million shares!!

Yup, it increased yet again. Which means based on this enlarged share base, Scomi's current eps is now 15.2 sen. Ok?

And yes, I had mentioned the perils of a company issued placement shares.

Currently, Scomi does have the earnings to justify its strategy but do remember what happened back then in Sept 2005. Look at how the share tumbled when the earnings wasn't there. Do take note of this issue. It could well happen yet again but then on the other hand, if the Scomi 'produce' those earnings, the market could well go ga-ga over the share again.

Cheers!

<===============>

19th Aug 2006

Scomi reported its 2006 Q1 Earnings on 25th May 2005.

Quarterly rpt on consolidated results for the financial period ended 31/3/2006

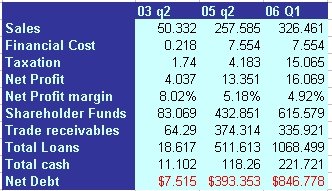

The following table simple table says it all. There different point of time to highlight the progress of Scomi Group as a company.

Look at the sales and net profit numbers.

Yes, the sales and net profit has increased a lot but do you see any creation of wealth?

Back then, 03 Q2, Scomi Group was a simple stock earning 4.037 million for the quarter. But it's net debt was a mere 7.515. Very manageable.

Today Scomi? 06 Q1, Scomi Group is now a complex Godzilla, earnings some 16.069 million for the quarter, which is about 4 times more than it earned back in 2003 Q2. Fantastic. Bravo. But just look at the cost of such engineering of wealth. Scomi Group is now in a nett debt positiion of $846.778 million.

How?

0 comments:

Post a Comment